We All Know This Ends With QE

But The Path Requires Pain First

Banks Are The Tip of The Iceberg

After a volatile month, the S&P 500 and Bitcoin both ended March up 3.5% and 23%, respectively. The story of the month of course was the collapse of Silicon Valley Bank, Silvergate Bank, and Signature Bank. As a result of the banking scare, the Federal Reserve Bank and U.S. Treasury announced a joint emergency funding program called the Bank Term Funding Program (BTFP). The BTFP is a program that allows commercial banks to pledge their U.S. Treasuries (USTs) and agency mortgage-backed securities (MBS) as collateral (valued at par) to receive a 1-year loan to satisfy any potential run on deposits.

The BTFP is a bandaid on a much larger problem. Over the past decade, commercial banks have been hyperregulated by the U.S. government to hold USTs when interest rates were low. However, when the Fed began aggressively raising rates in 2021, the value of bank-held USTs began to materially fall in value, causing bank balance sheets to be undercollateralized relative to their loan books. In the case of Silicon Valley Bank (whose depositor base was ~90% uninsured), this struck fear in corporate depositors and led to a panic withdrawal from the bank. To be clear, Silicon Valley Bank had idiosyncratic issues and we do not expect a bank run to be a material fear for everyday people.

The Fed and U.S. Treasury’s quick actions have severe implications for the current business and market cycle:

Fed emergency lending programs are NOT QE. While Bitcoin and risk assets exploded higher following the BTFP, there is a significant difference between bank loans (not QE) and the Fed printing money to purchase USTs and MBS (QE).

U.S. commercial bank deposits are now declining at one of the fastest rates ever following the March banking crisis in search of safer, higher-yielding stores of value – aka U.S. Treasuries.

As a result of depositors withdrawing their money and moving to USTs, commercial banks have already begun slamming the brakes on lending activity, which will soon be a net drag on the U.S. economy.

Our view is that U.S. banks will be nationalized over time as we continue to spiral into a long-term debt crisis triggered by structurally higher inflation.

Read enough monetary history and you know how this ends. The Fed will eventually cut interest rates and print trillions of dollars to *fix* (not avoid) a crisis…but the path will require PAIN first.

Source: 42 Macro

Base Case - Inflation Remains Resilient

Following the Fed’s BTFP, risk assets rallied, bond yields fell, and the Fed funds futures curve began pricing in immediate interest rate cuts. Many pundits have recently begun calling for the Fed to pause and begin cutting interest rates, seemingly forgetting that unemployment is at 50-year lows and underlying inflation is still compounding at 2-3x the Fed’s price stability mandate.

Let me repeat this for everyone trying to front-run QE…the Fed WILL NOT cut interest rates and launch QE with unemployment at 3.5%, median CPI (3mo SAAR) at 7.5%, and private sector labor income (3mo SAAR) growing 9.1%. The U.S. economy is still quite resilient. And while we do think the money printer is coming, investors need to wait for excruciating pain (market selloff) before the doctor (the Fed) administers the drugs (rate cuts + QE).

Source: 42Macro

That said, we are beginning to see cracks in the labor market. U.S. initial jobless claims ticked up sharply this past month to +238k jobs. The JOLTS data also showed that there are now 1.7 job openings per unemployed worker, down from the high of 2.0 jobs/worker last month, suggesting fewer job openings as companies pull back from hiring. It’s important to remember one data point doesn’t make a trend, however, if we look back in history, sharp increases in U.S. initial jobless claims and continuing jobless claims have coincided with recessions (red bars).

Finally, we will remind investors that the Fed’s most recent summary of economic projections expects the U.S. unemployment rate to rise by 100 bps (to 4.5%) in the next 9 months – an increase that we’ve only seen during previous recessions. Effectively, the Fed (as they’ve been signaling for months) is predicting a recession driven by a weaker labor market. The Fed’s objective is to break the U.S. economy and labor market so we can bring inflation back down to 2%. Keep your eye on the prize.

Source: 42 Macro

Bull Case - The Rising QE Narrative

The post-2008 market environment has been characterized by two main narratives: 1) buy the dip, and 2) don’t fight the Fed. Like addicts, investors have been so conditioned to the Fed’s reaction function of QE and rate cuts that any hint of a crisis is immediately followed by rabid market buying to front-run the drugs. This past March was more of the same. And while the Fed’s balance sheet did expand to accommodate the emergency loan program, history would suggest that emergency loans typically precede market selloffs. Our view is that the BTFP will give the Fed cover to focus on its real objective, which continues to be fighting inflation.

Source: 42Macro

By now, most investors understand that net liquidity is a main driver of asset markets. However, net liquidity is a function of 1) the Fed’s balance sheet, 2) the reverse repo facility, 3) the treasury general account, and now 4) emergency lending programs. While net liquidity has risen over the past several weeks due to the introduction of emergency loans, we estimate net liquidity will face serious headwinds once we get past the U.S. debt ceiling in 2H23. Specifically, #2, #3, and #4 will all reverse as we move through the rest of the year, not to mention the ongoing quantitative tightening that is still occurring in the background. Taken through the lens of the phase 1 liquidity cycle downturn, we believe risk assets will eventually get the memo, and buy-the-dip investors will be wiped out in 2H23.

Source: 42Macro

Bear Case - Beware the Credit Cycle Downturn

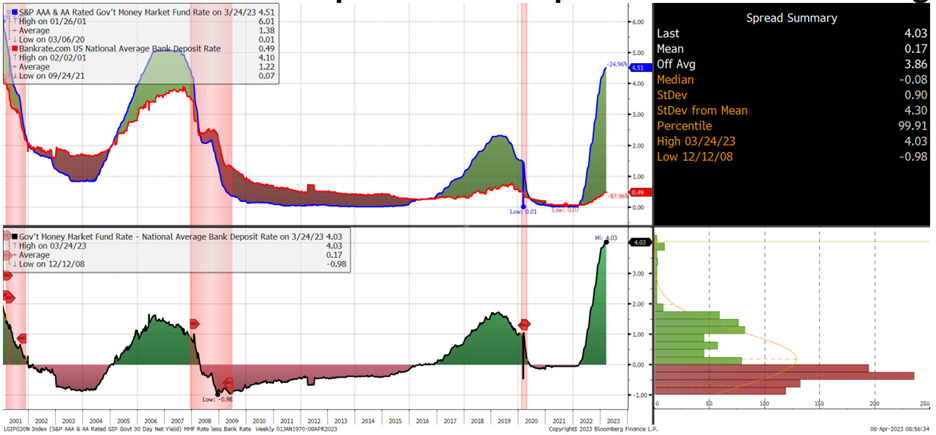

But wait, there’s more. For over a year, we’ve been pounding the table on the liquidity cycle downturn, but it’s the phase 2 credit cycle downturn that keeps us up at night. Investing (and saving) is all about opportunity cost. With the U.S. national average bank deposit rate at 0.49%, why would you keep your money in a bank when: 1) there are *perceived* issues at several commercial banks, and 2) you can make 4.5% or more with USTs. This ~400 bps spread between bank deposits and UST yields is the largest we’ve seen in over 2 decades. And now with the proliferation of mobile banking, it’s no wonder why commercial banks are quickly seeing the largest deposit outflows in recent history.

Source: 42Macro

As a result of deposit outflows, “small” U.S. banks (which make up ~40% of total U.S. commercial bank loans and leases) are now beginning to see their total assets contract for the first time in years. As bank assets decrease, their lending activity must also contract. In fact, in less than 1-month post-BTFP, small banks have already begun to see overall loans & leases slowdown materially. This is by far the biggest red flag we’ve seen to suggest the phase 2 credit cycle downturn may be in the process of being pulled forward from our previous call of late 2023. If the Fed continues to raise interest rates (which we think is likely), bank deposits will continue to flow toward USTs, causing commercial banks to curtail their lending activity, which will slow the real U.S. economy – exactly what the Fed wants.

Source: 42Macro

Don’t Be A Hero and Front-Run QE

For all the investors getting excited about the pause pivot and trying to front-run QE, you should study history. The only two examples of interest rate pause-pivots have been in July 1942 and January 2019 – both of which were bullish for asset markets but also did not have a looming recession around the corner.

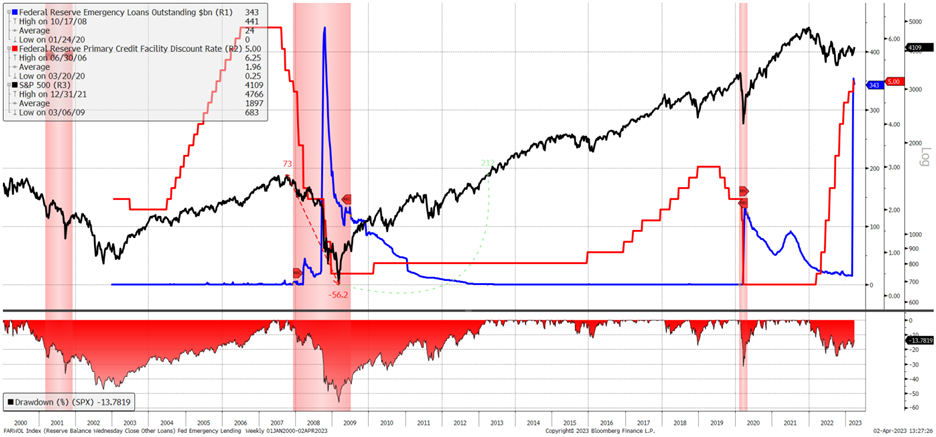

As an example, if we look at 2007 when the Fed was cutting interest rates ahead 2008 crisis, asset markets were falling (black line) from mid-2007 to late 2008 as the Fed cut interest rates (red line) to 0%. It wasn’t until March 2009 that the market bottomed…right after QE began (blue line). The same dynamic also occurred in March 2020, although on a much more compact timescale given the speed of the crisis.

Source: 42Macro

My final takeaways:

It’s not bullish when the Fed begins cutting interest rates into the teeth of a recession. Quite the contrary – it means the Fed is frightened they overtightened monetary policy (likely true already) and is a leading indicator of pain (market selloff) to come.

The investable inflection in the liquidity cycle will only occur after the Fed’s holdings of USTs and agency MBS increase through quantitative easing (we are still doing QT by the way).

Every investor knows QE is coming. Don’t be a hero and front-run it without understanding the path. We will not get the “money printer go BRRRRR” without the pain FIRST. If you believe the new bull market has started, you are impliclty betting on the Fed to achieve a “soft landing” of the U.S. economy…a statistically improbable event.