Transitory Goldilocks

New Bull Market or Bull Trap?

The FOMO Is Strong

2023 has gotten off to a strong start, with the S&P 500 (+6.2%) and Bitcoin (+39.9%) both reclaiming their 200 day-moving-averages. While we’re no strangers to bear market rallies, it is curious the market coiled up so aggressively to start the year following an unequivocally hawkish Fed meeting in mid-December. However, we suspect two key factors have recently weakened the USD and temporarily flattered global net liquidity: 1) the U.S. Treasury offsetting quantitative tightening ahead of the U.S. debt ceiling and 2) China reopening and ending their zero-COVID policy.

We now find ourselves in a particularly awkward stage of the business cycle that some are calling transitory goldilocks. Recall, GOLDILOCKS is one of 4 macro regimes we follow that occurs when growth is accelerating and inflation is decelerating. In a typical hiking cycle, we usually see the following playbook occur: 1) Fed hikes interest rates, 2) economic activity contracts, 3) the labor market weakens, and 4) inflation moves lower. What is unique, however, is that the disinflation process has begun before #2 and #3, causing investors to optimistically view that the worst is behind us.

With financial conditions having loosened materially over the past several months, we would note an immaculate disinflation process back to 2% is historically unachievable without a slowdown or contraction in growth. That said, markets will cling onto whichever narrative they can until the hard data says otherwise. By 2H23, we expect net liquidity to inflect lower and the conversation will once again be about recession. Until then, investors and traders may chase the market higher due to FOMO (ie/ career risk).

Source: Bianco Research

Base Case - Higher For Longer

There is no denying since 4Q22 we’ve seen an immaculate disinflation in headline and core inflation. Historical evidence suggests this rate of disinflation is only achievable alongside contracting GDP growth, which was not the case in 4Q22 (+2.9%). This combination of accelerating growth and decelerating inflation results in a GOLDILOCKS macro regime, which is statistically a risk-on environment.

Looking under the hood, the immaculate disinflation process seems to be mostly driven by transitory inflation in goods, as the supply chain disruptions from COVID are now behind us. That said, key measures of underlying inflation are still compounding at rates well north of the Fed’s 2% target, which in the words of the great Kobe Bryant suggests the ”job’s not finished.”

Source: 42 Macro

We would also remind readers that the Fed recently upgraded the labor market in its reaction function instead of inflation in the December FOMC meeting. While the Fed is still fixated on inflation metrics, a resilient U.S. economy (evidenced by the labor market) will likely cause the Fed to overtighten monetary policy out of fear of a wage-price spiral.

The most recent JOLTS data out last week showed a re-acceleration in labor market tightness, with there now being 1.9 job openings for every unemployed worker. Furthermore, non-farm payrolls from last week also showed the creation of 517K new jobs (significantly ahead of economist estimates of +188K), as the unemployment rate fell to 3.4%, the lowest since 1969. This is an incredibly difficult situation for the Federal Reserve. As long as the labor market remains tight, workers will have the leverage to demand higher wages. Higher wages beget higher inflation, and higher inflation beget tighter monetary policy, which will push the U.S. economy closer to the edge of recession.

Source: Bianco Research

As a result of the re-acceleration in non-farm payrolls last week, Fed fund futures are now pricing in a 96.7% chance of a 25 bps hike in March and a 74.0% chance of a 25 bps hike in May (up from ~30% the week before). This re-rating of Fed fund futures higher is significant and will likely weigh on risk assets if these probabilities continue to rise from strong economic data. Recall, the bull case was that we fall into a recession quickly and the Fed begins cutting rates as early as June 2023, though this view is quickly changing. This is in stark contrast with the Fed’s estimate that they won’t cut rates until 2024 at the earliest, a view that is beginning to finally be priced in as shown in the table below.

One must wonder, if there was a real recession, why would the Fed only cut by ~25 bps by the end of the year? This implies the bull case was an immediate recession + soft landing by the Fed. Given how markets are pricing in Fed fund futures, we would take the over. We believe the Fed will raise interest rates higher than current expectations, and we do not expect them to cut rates until we are convincingly in an actual recession. Remember, the Fed by mandate is responsible for managing not just the current business cycle, but all the business cycles in the future and will do what it takes to reign in long-term inflation expectations.

Source: CME Fed Watch Tool

Upside Risk - Soft Landing

The January rally in risk assets (equities and crypto) looks like the upside risk of a soft landing is becoming fully priced in by financial markets. Specifically, net liquidity dynamics inflected materially higher to start the year catalyzed by the U.S. Treasury, which is draining the Treasury General Account (TGA) ahead of the U.S. debt ceiling deadline in June 2023. This action by Secretary-Treasurer Janet Yellen is effectively offsetting the Federal Reserve’s quantitative tightening efforts. We believe this dynamic will fully reverse by mid-year after the debt ceiling is resolved by U.S. Congress, causing the U.S. Treasury to re-fill their TGA while the Fed continues QT, initiating a double whammy on net liquidity to the downside.

Furthermore, the reopening of China and initiation of fiscal stimulus to encourage demand has already begun flattering Chinese and European economic activity. Recall, as the second largest economy in the world, China has a massive influence on global economic activity and may cause the global economy to remain more resilient. However, as we discussed before, good economic data may overheat the global economy and cause a re-acceleration in inflation, giving cover for Central Banks to continue tightening monetary policy. In the meantime, however, we believe the China reopening may keep the global economy in a transitory goldilocks period for the next quarter or so, but we wouldn’t be too quick to declare the bottom is already in.

Based on our analysis of prior bear market rallies in the S&P 500, the median BMR lasts 2 months, rallies 18%, and retraces 75% of the prior leg down. The current BMR, which began on 10/12/22 has lasted 4 months, rallied 17%, and retraced 83% of the prior leg down. This would put a cap on the current BMR at around $4,200 on the S&P 500. Now of course, we could always go higher, especially given how unique of a bear market this has been, but we believe we are approaching the upper limits of how high this market can go, given our medium-term outlook for DEFLATION and negative net liquidity by mid-year.

Source: 42 Macro

Downside Risk - Imminent Recession

Given the long and variable lags of monetary policy, the Fed may have already committed a policy mistake and when we look back on this period, the NBER may declare we were already in a recession by January 2023. When looking at data going back to the 1950s, nominal employee compensation (wage growth) on a 3-month SAAR basis typically inverts below the Fed funds rate during recessionary environments. 6 of the past 9 inversions happened during an actual recession, and 3 of the past 9 inversions saw a recession within 6 months. We inverted again for the 10th time in December 2022. On a median basis, the Fed has historically cut interest rates by 25 bps 3 months after inversion and cut 100 bps 6 months after inversion, however, this current Federal Reserve is still raising interest rates! We believe the historically tight labor market due to a structural shift lower in labor participation from COVID is putting the Fed in a precarious situation.

Source: 42 Macro

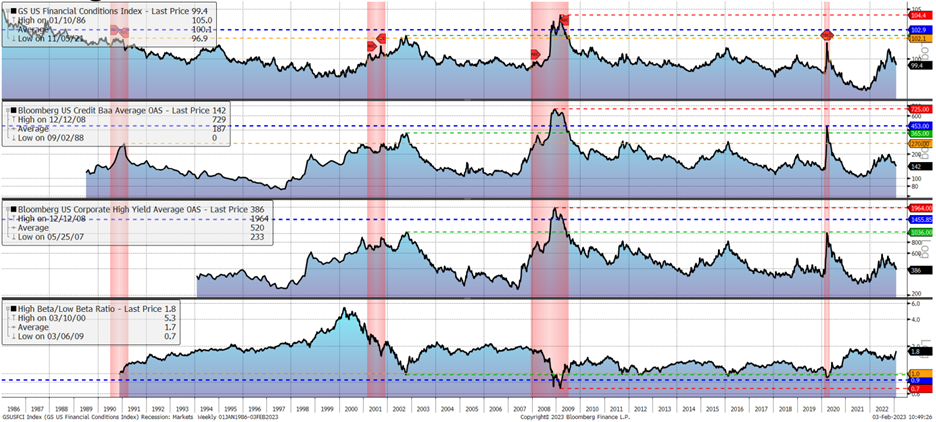

Furthermore, bulls argue that the market already bottomed in 2022 after the recession was fully priced in – a notion that we vehemently disagree with. As we’ve said in our last letter, the weakness in 2022 was a function of the phase 1 liquidity cycle downturn, but markets have not gotten close to pricing in the phase 2 credit cycle downturn. When we compare U.S. financial conditions, credit spreads, and high beta/low beta stock ratios to prior recessions, we conclude financial markets are still in la-la land. For perspective, the chart below shows the 2008 Great Financial Crisis in red, the 2001 Dot-com bubble in green, the 1990 recession in orange, and the mean of all three recessions in blue. The fact high beta stocks are 1.8x more expensive relative to low beta stocks when recessions typically see this number below 1.0x is all you need to know to understand how aggressive markets are mispricing the macroeconomic environment.

Source: 42 Macro

Bitcoin, Wen Moon?

While we, unfortunately, did not buy BTC after the FTX collapse due to fears of contagion risk, we are still unconvinced that the bottom is fully in. That said, we want to update our views on Bitcoin specifically, given it remains our favorite macroeconomic asset to own in our lifetime. With BTC now trading around $23K, we have reclaimed the STH cost basis ($18.9K), aggregate realized price ($19.8K), and the LTH cost basis ($22.3K). Given the uniqueness of this economic cycle, there is a risk of going much lower but owning BTC at its realized price (the gold line in the chart below) has historically been a stellar investment across any multi-year timeframe. We are currently selling puts to accumulate BTC anywhere in the $19K-$22K range but will keep extra cash on hand for when the phase 2 credit cycle downturn likely starts in 2H23.

What gives us pause however for not chasing this rally is that shitcoins like SOL (+140%), FTM (+210%), APT (+380%), etc. have all rallied exuberantly YTD. Even crypto companies like COIN are up over 100%. To us, it’s never healthy to see a short squeeze rally with high beta risk assets significantly outperforming more established low-beta companies and blue-chip cryptos like BTC (+41%) and ETH (+40%). Our advice would be to accumulate BTC on a pullback but to be wary of chasing explosive moves higher. We suspect the bulls dancing on bear graves will soon find themselves in the same plot of dirt later this year.