The Fed Did Not Pivot

Markets Are Mispriced Following July Fed Meeting

In July, U.S. stocks had their best month in two years despite continued discouraging growth and inflation data. During times like this, it’s important to remember that markets don’t move in straight lines, they dance. Following the July FOMC meeting, investors became remarkably optimistic that the Federal Reserve won’t tighten monetary policy much further, and will instead pivot to looser monetary conditions – a view we strongly disagree with, as we explored in last month’s letter Global Recession is Inevitable.

With leading indicators for global growth weakening considerably, we’re quickly approaching the point in the global Central Bank reaction function that historically would lead to a pivot in monetary policy. However, this time is different. Politically, global Central Banks will not ease monetary conditions while inflation momentum is still accelerating. Recent wishful thinking from investors will soon be met with the reality that not only is economic growth showing signs of contraction but also that Central Banks will be more hawkish than anticipated.

With that backdrop, let’s jump into our economic and market outlook.

Outlook (TLDR)

Short Term (< 1 month)

Our research suggests we’re in the middle of another vicious bear market rally (similar to the one in late March), fueled by two key items: 1) overly bearish market positioning headed into 2Q earnings season (which did not disappoint quite nearly enough), and 2) the removal of forward-guidance on interest rate increases from the Fed, confusing markets into believing a Fed pivot is near.

As a result, the S&P 500, Nasdaq, Russell, Bitcoin, Ethereum, and Gold have been overbought across our fractal momentum for the better part of the last month. Similarly, the USD, 10-Year UST, High Yield Credit Spreads, and Equity volatility (VIX) have spent most of the month in oversold conditions. While these moves may have further room to go, we believe there is a complacency among investors and fundamental mispricing of many asset classes given the deteriorating macro-outlook.

We continue to believe with high conviction that the bottom in risk assets is not in and that the Fed will continue to overtighten monetary policy given inflation momentum continues to build while the labor market remains strong. Recent commentary from Fed Presidents has already begun to walk back Powell’s “dovish” comments from the July FOMC meeting, suggesting interest rates will likely be higher for longer, as the Fed’s fight with inflation is “nowhere near almost done.”

As has been the case for most of this year, we would use this recent strength in markets to take down risk exposure and/or initiate a short position on risk assets.

Medium Term (2-6 Months)

As it relates to our top-down MARKET regime and bottom-up MACRO regime, we believe markets are significantly mispriced, unrealistically anticipating a Fed pivot and/or “soft landing.”

Based on our MARKET regime analysis, 31% of global assets are pricing in a REFLATION (growth accelerating, inflation accelerating) regime vs. 28% INFLATION and 24% DEFLATION – signaling to us that the market is confused.

This is in stark contrast to our MACRO regime analysis, which predicts a 61% chance of DEFLATION (growth decelerating, inflation decelerating) and a 3% chance of REFLATION over the next 6 months. As such, we believe the current strength in risk assets is being fueled by a REFLATION hope that is unlikely to materialize given the obvious slowdown in global growth and likely peaking of inflation eventually.

Source: 42 Macro

The last time we saw REFLATION emerge as the dominant market regime with no fundamental macro support was in early January and early April of this year, which if you recall led to significant losses for investors who chased the REFLATION trade on the long side.

Source: 42 Macro

Our call against REFLATION is supported by the first batch of July Manufacturing PMI data which suggests the global goods economy is beginning to slow quickly, particularly in Europe, China, and Mexico, where the data is beginning to contract. In the U.S., headline consumption (Real PCE) of 0.2% continues to grind to a halt as excess savings (now at 5.1%, the lowest since August 2009) cannot weather the building inflation momentum.

We find it extremely improbable the Fed will pivot monetary policy into an inflation spike given Fed Chair Powell’s comments at the July FOMC meeting:

“We're going to be focused on getting inflation back down. And we-- as I've said on other occasions, price stability is really the bedrock of the economy. And nothing works in the economy without price stability.”

As a result, we wouldn’t expect a Fed pivot until inflation is showing “clear and convincing” evidence of coming down. Historically, recessions have had a 100% success rate at reducing inflation quickly, and we believe the Fed is trying to secretly engineer a recession as per Powell’s comments:

“We think it's necessary to have growth slowdown. We actually think we need a period of growth below potential, in order to create some slack so that the supply side can catch up. We also think that there will likely be some softening in labor market conditions. And those are things that we expect, and we think that they're probably necessary if we were to <reduce> inflation.”

While we do think the Fed will eventually pivot monetary policy, we think it’s impossible as investors to front-run the liquidity, growth, and inflation cycles. The global growth slowdown hasn’t even begun to be priced into markets, which we think will be the next downside catalyst to make new lows. We believe inflation won’t break until growth breaks (per Powell’s comments), and until then, the Fed is likely to remain very hawkish in its monetary policy to engineer a recession. As such, we remain bearish on risk assets but remain cognizant that a real Fed pivot (pausing or cutting interest rates) will likely be very bullish for risk assets.

Long-Term (6-12 Months+)

Netizen’s investment thesis is that the fiat currency world, supported by debt and political power, will shift towards market-based money, as has always occurred at the end of empires. We believe the Great Power competition between the West (U.S., Europe, Japan) and East (China and Russia) will result in the unraveling of the Petrodollar system that was established in 1971 after the U.S. defaulted on their international gold obligations. Over the coming years, national self-interest will likely continue to drive wedges in geopolitical relations, especially between commodity-producing nations (like Russia) and hyper-financialized economies (like the U.S.).

As we reflect on current events, we view the recent tension between U.S., Taiwan, and China as a harbinger of more geopolitical conflict to come. Specifically, last week U.S. House Speaker Nancy Pelosi antagonized Chinese leaders by visiting Taiwan’s President Tsai Ing-wen, calling the visit a “commitment to supporting Taiwan’s vibrant democracy.”

Source: Twitter

According to China, Pelosi’s visit to Taiwan violated the One China policy, a cornerstone of Sino-US relations that was established by the Nixon administration in 1972. Recall, that Taiwan has been independent of China since 1949 following a civil war, however, Beijing views the island as part of its territory, and hopes to eventually unify Taiwan with the mainland, using force if necessary.

Following Pelosi’s visit – China announced live-fire military exercises surrounding Taiwan as a show of force. In addition, China has already begun sanctioning Taiwan and cut off communications with U.S. military leaders. While this is still an unfolding story, we believe China’s brewing conflict with Taiwan builds on top of Russia’s invasion of Ukraine as more evidence of the changing world order.

We continue to believe we’re headed for a global monetary re-ordering that will likely see the fall of the U.S. empire and the death of the Petrodollar as a function of the Great Power competition between the West and East. We view non-fiat energy-related assets such as Bitcoin, energy, agriculture, metals, and commodity-related infrastructure (ie/ real things) will be the best stores of value AFTER the coming deflationary recession.

The Fed Will Break The Economy

Bullish investors rejoiced after the July FOMC meeting following Powell’s dovish comments:

“We are now at levels broadly in line with our estimates of neutral interest rates, and after front-loading our hiking cycle until now we will be much more data dependent going forward.”

Recall, that the neutral rate is a conceptual interest rate that neither pushes economic activity higher nor slows it down. For months, the Fed has signaled to investors they will raise interest rates into restrictive territory, meaning that any incremental interest rate increase after today should in theory slow the economy.

That said, the removal of forward guidance and shift toward data dependency fueled optimism from bulls that the Fed is now closer to pivoting than they were several months ago. We think this view is inconsistent with the Fed’s price stability mandate, which would require highly restrictive interest rates to fight inflation. As such, we think the market consensus is improperly anticipating a Fed pivot, and we would not be chasing the recent rally.

Source: The Macro Compass

2.5% Is Not the Neutral Rate in 2022

Last week, former Treasury Secretary Lawrence Summers accused the Federal Reserve of wishful thinking regarding how high interest rates will need to go to bring down inflation from four-decade highs:

“Jay Powell said things that, to be blunt, were analytically indefensible. There is no conceivable way that a 2.5% interest rate, in an economy inflation like this, is anywhere near neutral.”

We agree with Larry. As we look at the most recent inflation data and compare it to the 5-year trend ending in 2019, it’s clear our current economy is inflating at least three times faster than normal. Specifically, trimmed mean PCE inflation, median CPI, sticky CPI, and core PCE inflation continue building momentum on a month-over-month basis.

We’re genuinely confused why Fed Chair Powell said 2.5% was the neutral rate in the most recent July FOMC meeting, considering he said the neutral rate was 2.5% back in 4Q18 when inflation was only 2%.

While it’s difficult to estimate the economy’s neutral rate (all the PhDs at the Fed can’t even do it), we think it’s safe to say the current neutral rate is at least in the 3%-4% range if not higher, suggesting that the Fed will need to increase the Fed funds rate well past 3%-4% (currently at 2.25%-2.5%) if it wants to kill inflation (priority #1).

If the Fed revises its estimate for the neutral rate higher in the coming months, investors will interpret this as incrementally hawkish, which will likely take the “Fed pivot” narrative off the board and stop the current optimistic bear market rally in its tracks. Beware. A higher revision of the neutral rate would cause Fed fund futures to re-rate higher, catalyzing further weakness in long-duration risk assets (tech, crypto, etc.)

Source: 42 Macro

Strong Labor Market = Hawkish Fed

With 2Q22 GDP (-0.9%) confirming a technical recession, the White House and Federal Reserve have denied an actual recession, citing strength in the labor market as disconfirming evidence. While there has been a recent uproar on social media about how policymakers are changing the definition of a recession, we believe the No Recession narrative from U.S. leaders provides the Federal Reserve political cover to continue tightening monetary policy aggressively before we do hit an actual recession.

In our view, last Friday’s jobs report gave the Federal Reserve carte blanche to be as hawkish as they need to be in the coming months, as nonfarm payrolls of +528k jobs obliterated estimates of +250k.

Looking underneath the hood, the Employment Cost Index (which is the broadest measure of employee wages, benefits, and compensation) grew 5.5% (an all-time high), suggesting a wage-price spiral may contribute to future inflation momentum. Furthermore, with 1.8 job openings per unemployed worker and a 3.1% quits rate (both near all-time highs), this suggests the labor market is as tight as it has been in recent history.

Following the strong jobs report, Fed fund futures repriced higher, suggesting a 68% probability of a 75-bps interest rate increase in September up from a 28% probability last week. Not only is the Fed not pivoting, but the bond market is now anticipating a higher likelihood of a hawkish outcome relative to last week. If the CPI (inflation) report on 8/10 shows no signs of inflection lower, we would expect the probability of a 75-bps hike to continue increasing, which would be incrementally bearish for risk assets.

Source: 42 Macro

The Only Way Out of Inflation Is Recession

In the June FOMC meeting, the Fed provided their summary of economic projections calling for core PCE (their preferred inflation metric) to be 2.7% by year-end 2023 (down from 4.3% in 2022). Given that date is now only 16 months away, history would suggest that it’s unlikely the Fed will be able to achieve its inflation targets without causing an actual recession.

If we look at historical core PCE data going back to 1960, we have never seen a 210-bps decline in core PCE over an 18–24-month period without inducing an actual recession. Also, keep in mind that core PCE of 2.7% is still 70 bps ABOVE the Fed’s long-term target of 2% inflation, implying the Fed must engineer significant demand destruction in the economy if they want to get inflation under control. With June Real PCE (consumption) grinding to a halt (now 0.2% on a 3-month SAAR vs. 0.8% last month on a 3-month SAAR), we believe the demand slowdown is already underway.

Fed Chair Powell’s rhetoric since November 2021 suggests we’re operating with a new Fed regime that prioritizes lower inflation at the expense of growth. However, we suspect their resolve will be tested in the coming quarters to see how serious they are about achieving price stability. While we are positioned negatively on risk assets in anticipation of an actual recession, we suspect the Fed will eventually cry “mercy!” and pivot to intervene in the economy, as they have done for decades.

Source: 42 Macro

U.S. Manufacturing Already Pointing to Recession

Speaking of engineering recessions, last week we received incremental evidence that the U.S. Manufacturing sector may already be in an actual recession. The last four times (1973-1975, 1980, 2008-2009, and 2020) the spread between new orders and inventories in the ISM Manufacturing Index was this negative, the U.S. was already in a recession. In addition, the recessions seen in 2001, 1990-1991, and 1981-1982 never had a negative spread this low. Historically, a -9.3 spread implies a sub-40 ISM (above 50 is growth, below 50 is contraction), which would be on par with the 2008 recession.

Given the global slowdown and contraction in July Manufacturing PMI data, we would expect manufacturing to continue to slow in the coming months, which would be the nail in the coffin to confirm an actual recession. However, in the meantime, the Fed will use the labor market strength as cover to maintain a hawkish policy stance.

Source: Compound Capital Advisors

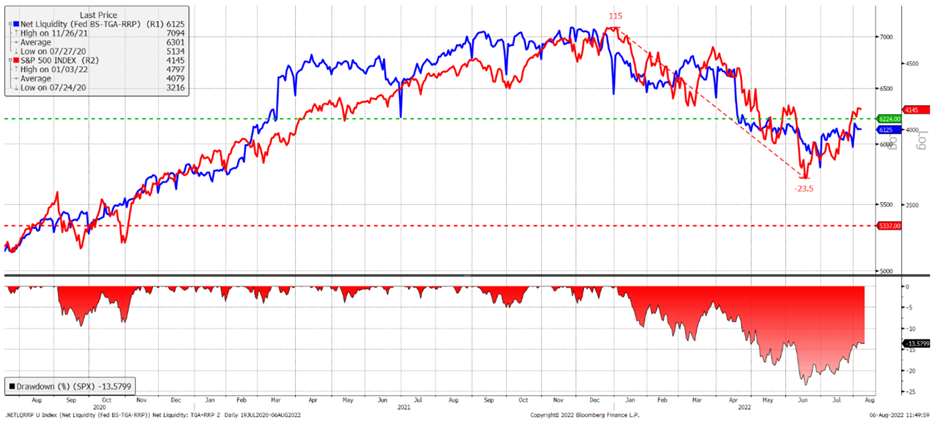

Net Liquidity Drives Markets

As we think about where markets are headed from here, it’s important to understand that net liquidity drives markets. Excess liquidity pushes asset prices higher (and may lead to higher inflation as an unintended consequence) while draining liquidity causes markets to go lower (which through the negative wealth effect slows down demand and growth).

Net Liquidity can be defined as a function of three items:

Federal Reserve Balance Sheet (Fed BS) minus

Treasury General Account (TGA) minus

Reverse Repo Facility (RRP)

With current net liquidity at $6,125 billion, we estimate the fair value for the S&P 500 is around $4,000. However, given the Fed’s guidance around quantitative tightening (QT), we expect the Fed to reduce its balance sheet by $428 billion through year-end.

Meanwhile, we expect the TGA to remain relatively stable at $554 billion with a floor of $500 billion, given Treasury Secretary Janet Yellen’s implicit guidance from last week's Quarterly Refunding Announcement.

Finally, we expect the RRP to increase (which would be negative for net liquidity) as the Fed continues to raise interest rates past a soon-to-be-revised-higher neutral rate. Using the 3-month annualized rate of change and month-over-month rate of change we come up with two scenarios. Using the former, our base case is that the RRP will increase by $361 billion by year-end, and using the latter, the bull case (which we view as unlikely given the Fed’s hawkish stance) is that the RRP will decrease by $526 billion by year-end.

Putting this all together, our base case (which we view as a high probability outcome) is that net liquidity will decrease ~$788 billion through year-end, which would imply $3,400 on the S&P 500 (-18% from current levels). The bull case (which we view as a low probability outcome) is that net liquidity will increase ~$99 billion through year-end, which would imply $4,100 on the S&P 500 (-1% from current levels).

Either way, we view the current market as overbought, and we would be sellers and/or shorting risk assets at these levels. We do not believe in the false narrative that the Fed is about to pivot anytime soon.

Source: 42 Macro

Bitcoin Is a Hedge on Global Liquidity

As a long-time advocate of Bitcoin who is secularly bullish on the asset while also being cyclically bearish, we want to dispel a common misconception about the world’s most important asset.

There are three types of inflation:

Monetary inflation – growth of the broad money supply

Asset price inflation – growth in the price of financial assets like stocks, bonds, gold, real estate, etc.

Consumer price inflation – growth in the price of everyday goods and services (which is how most people think about inflation)

Saying Bitcoin is an inflation hedge is woefully reductionist. What type of inflation? Generally, when people say this, they’re talking about consumer price inflation. But as we’ve learned over the past 9 months, Bitcoin is down over 60% despite higher and accelerating inflation.

The reality is that Bitcoin is a hedge against monetary inflation or growing money supply. And with global Central Banks tightening monetary conditions in unison (led by the Fed which has by far been the most aggressive given we control the global reserve currency, the USD), money supply growth has been decelerating for over a year. As well, a strengthening USD (due to hawkish Fed monetary policy) also weighs on money supply growth when global Central Bank liquidity is then translated back into USDs.

As a result, we’ve been bearish on Bitcoin all year despite it being our favorite asset to own in the long run. And while we’re currently near what has historically been a cyclical bottom in global money supply growth (denominated in USD), we still believe there is more tightening ahead of us and that the USD has more room to strengthen, which would continue to put pressure on Bitcoin.

Source: MrBlonde Macro

The Bottom Is Not In

The most common (and arguably important) question investors are grappling with is “Is the bottom in?”

If we look at the last 13 bear markets going back to 1957, we can begin to triangulate an answer.

The median drawdown for a bear market is -28%, which is slightly worse than the -24% drawdown the S&P 500 troughed at on June 17. That said, we’ve seen bear market drawdowns as bad as -57% and as shallow as -19%.

More importantly, the S&P 500 historically bottoms 1 month AFTER the Fed pivots. In fact, it’s very rare that markets bottom BEFORE the Fed pivots and most Fed pivots are followed by more selling despite an inflection in the liquidity cycle. Given our view that we are at least several months away from a Fed pivot (considering the momentum of inflation), it’s unlikely the market has bottomed.

Finally, the S&P 500 historically bottoms 3 months BEFORE a trough in the ISM Manufacturing PMI data, signaling an inflection in the growth cycle. Given that global ISM Manufacturing data is just starting to roll over, it’s unlikely we are anywhere near a trough in the growth cycle, signaling to us that the bottom is not yet in.

Putting this all together, we would expect to see the S&P 500 (and risk asset more broadly) bottom:

AFTER a Fed pivot (signaling an inflection in the liquidity cycle), but

BEFORE a trough in ISM Manufacturing PMI data (signaling an inflection in the growth cycle)

Given the 2022 Fed reaction function depends on the inflation cycle, we would also add that markets won’t bottom until AFTER inflation begins to roll over in a “clear and convincing way” which would trigger a Fed pivot (unless the Fed panics and pivots because of an exogenous event ie/ UST markets malfunction, war, etc.)

Source: 42 Macro

Final Thoughts

Bear markets are treacherous for both bulls and bears. Market psychology swings radically, pushing and pulling asset prices and positioning to extremes. During times like this, it’s important to keep a level head and have a quantitative research process. While we’re also susceptible to violent moves in prices, our process helps keep us a finger on the pulse of what’s really happening and how asset classes are likely going to evolve over time.

Below I’ve included a great chart outlining historical bear market rallies and how this one compares to the rest. The current bear market rally we’re experiencing has seen the S&P 500 rally 13.3% (as of 8/3/22) over 33 trading days. This puts us near the 90th percentile in terms of % performance and now the third longest bear market rally in history. Based on what we’ve outlined in this letter, we think we’re close to the top, but truthfully, the market will do what the market does.

Source: MrBlonde Macro

What we do know however is that eventually, consensus will come to the same conclusions that we’ve drawn – which is that:

The Fed is not about to pivot anytime soon,

we’re heading for a global recession,

the bottom for markets is not in.

We continue to believe right now is a good time to build cash and/or short the market if you are able.

We believe we’ll be rewarded with a generational buying opportunity once: 1) the deflationary recession is fully priced into asset markets and 2) the Federal Reserve pivots monetary policy and turns the printers back on.

Don’t Fight the Fed, and more importantly – don’t chase bear market rallies!

-Netizen Velez