In The Eye of The Macro Storm

The Credit Contraction Awaits

Global Liquidity Is Still A Headwind

Markets were less euphoric in April as the S&P 500 and Bitcoin both ended the month +1.5% and +2.7%, respectively. After an explosive 1Q23, risk assets are now consolidating as investors and traders decide if we’re at the start of a new bull run or in the eye of a macro bear market storm. The bullish cries for QE after the collapse of Silicon Valley Bank may indeed soon turn into bearish cries for help as another regional bank, First Republic, was acquired last week by none other than too-big-to-fail JPMorgan. In what seems to be another coerced government and private intervention, the Federal Deposit Insurance Corporation (FDIC) and JPMorgan stepped into what looks to be another band-aid to give the Federal Reserve cover to continue raising interest rates to fight inflation. I’m sure this will end well…

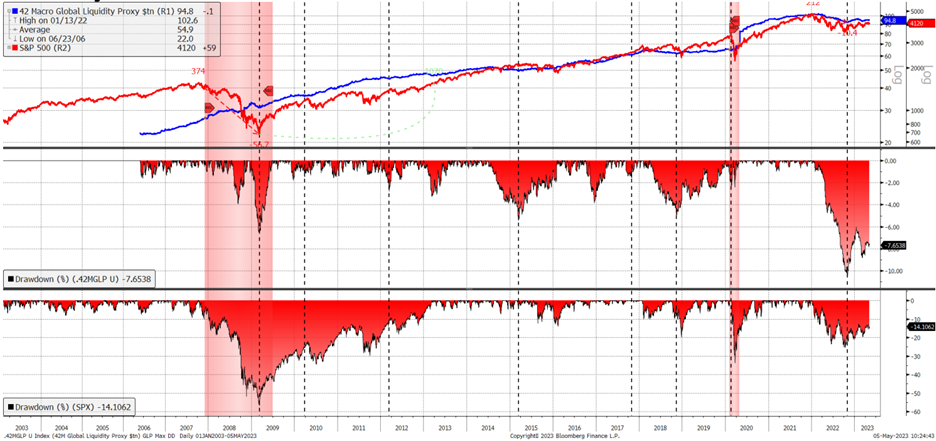

For the past year, we’ve been saying Phase 1 of the bear market would be a liquidity cycle downturn, which began in November 2021 when the Fed responded to persistent inflation with rate hikes and QT. However, recent actions overseas from the People’s Bank of China and the Bank of Japan led to a positive liquidity impulse in early 1Q23 which has given the illusion of the start of a new bull market. For those interested, we define global liquidity as global central bank balance sheet size + global narrow money supply + global FX reserves. The dotted lines below signify inflections in that metric, which often (not always) coincide with market bottoms.

Source: 42 Macro

That said, we’re not fully out of the woods yet. In March, we’ve seen a negative impulse in global liquidity, which may take the wind of the current bull market narrative. With the U.S. debt ceiling likely to be resolved in the next month, and China’s reopening underwhelming the global economy, we expect liquidity to become less of an important factor to asset markets in 2H23. Instead, we think the focus will shift towards credit contraction, which is already beginning to show in the data, which would lead us to Phase 2 of the bear market. It’s simply too early to declare victory over the bear market.

Source: 42 Macro

Base Case - Recession in Late 2023/Early 2024

We maintain our view that a global recession will likely commence in the 4Q23-1Q24 timeframe, though of course, recent issues in the regional banking sector may pull that risk forward. That said, the U.S. economy remains stubbornly resilient led by the services sector (82% of GDP and 86% of jobs). Despite the rising cost of living, U.S. consumer demand remains robust, as U.S. households have $5 trillion in checkable deposits and cash, the most in U.S. history. As a result, the U.S. housing market (which was beginning to show weakness due to rising mortgage rates) has been seeing a resurgence in recent months. All told these dynamics are why unemployment remains at a historic low of 3.4% and why inflation is persistently running 2-3x the Fed’s target.

Source: 42 Macro

Absent a recession, history shows that underlying inflation is all but guaranteed to remain resilient without further Fed tightening. Last week, the Fed raised its target interest rate again by 25 bps to 5.0% - 5.25%, in the face of yet another regional bank collapse. While the Fed believes regional bank issues will effectively constrain credit in the U.S. economy, it’s difficult to quantify the magnitude of tightening in terms of rate hikes. In their latest FOMC meeting, the Fed said they will take a data-dependent approach from here on out, meaning as long as the U.S. economy remains resilient, the labor market remains tight, and inflation remains persistent, the Fed will have zero reasons to cut interest rates.

Curiously, the bond market is pricing in expectations for an interest rate cut in September 2023, implying fear that something in the U.S. economy will break over the next several months. Recall, the Fed is projecting a 4.5% unemployment rate by the end of the year, and we’ve never seen a 110 bps increase in the unemployment rate in an 8-month window without a recession. Someone should tell asset markets that the Fed’s modal outcome is a recession.

Source: 42 Macro

Bull Case - A Weaker U.S. Dollar Would Reflate Global Growth

We believe we’re in the eye of the macro storm – caught in between the Phase 1 liquidity cycle downturn which for the most part is behind us, and the pending Phase 2 credit cycle contraction which is still at least a quarter or two away. In the meantime, asset markets can remain suspended in an alternate reality. What gives us the most concern is the risk of the excess long positioning in the USD unwinding, which could cause global growth to reinflate as global financing costs benefit from a weak dollar. Recall, as the global reserve currency, the world is structurally short USDs. 50% of cross border-loans and bonds issued are denominated in USDs. When the USD is weak, credit creation/borrowing becomes easier, therefore leading to positive economic activity.

Source: BIS

We’ve also noticed the breakdown in correlation between our U.S. liquidity proxy and the S&P 500, Bitcoin, and Ethereum. Once the U.S. debt ceiling dynamics are resolved, the U.S. Treasury expects to increase treasury bill issuance, which could effectively sterilize the Federal Reserve’s quantitative tightening. These crosscurrents are complicated, but this would only further weaken the Fed’s credibility in achieving its price stability mandate. And while treasury bill issuance may not be enough to offset the impending credit contraction, it could support asset markets in the interim. From our vantage point, it looks as if the Federal Reserve and U.S. Treasury are actively undermining each other in what seems to be an effort for the U.S. government to have its cake and eat it too (ie/ get rid of inflation without a recession).

Source: 42 Macro

Bear Case - Banks May Contract Credit

We continue to be concerned about the pending Phase 2 credit cycle contraction that may be at risk of being pulled forward given the recent regional bank issues. As we’ve discussed before, U.S. commercial bank deposits are declining at one of the fastest rates ever as customers flee towards higher-yielding U.S. Treasuries. Meanwhile, “small” banks are slamming the brakes on credit creation, particularly in commercial and industrial, commercial real estate, and consumer lending. If this activity continues to contract, we’ll likely see this manifest in slower real economic growth in the coming months which could pull forward our recession countdown.

Source: 42 Macro

Furthermore, we continue to believe that 2H earnings expectations are delusional. As a former sell-side research analyst, I can attest that banking research is a reactive profession. Sell-side analysts rarely lower earnings expectations proactively without getting confirmation from the company’s management team. However, by then, it’s often too late. The current Wall St. consensus is that earnings in 4Q23 and 1Q24 will grow 10% each quarter. This is exactly when we believe a recession will materialize, and it’s worth mentioning that we saw a similar dissonance occur in 2008 before the GFC. As we’ve said before, we’re in the eye of the storm, and asset markets are complacent.

Source: Bloomberg

Binance Under Investigation by DoJ

As much as the regional bank failures have highlighted the need for Bitcoin, it’s difficult for us to think this is the beginning of a new crypto bull market when the industry continues to be rife with fraud and criminal activity. On March 27, 2023, Binance and its CEO were sued by the CFTC over U.S. regulatory violations. In particular, the CFTC alleged in Federal court that Binance and its CEO, known as CZ, routinely broke American derivative rules and should have registered years ago. According to the CFTC complaint, there is clear evidence Binance was doing business with questionable Russia-linked entities. Specifically, when a Binance customer was found to have over $5 million of questionable transactions, Binance’s former Chief Compliance Officer Samuel Lim responded “Can let him know to be careful with his flow of funds, especially from darknet like Hydra. He can come back with a new account. But this current one has to go, it’s tainted.”

Last week, a Bloomberg article came out that Binance is now facing a U.S. probe of possible Russian sanctions violations. The Department of Justice’s national security division is looking at whether Binance or company officials violated sanctions related to Russia’s invasion of Ukraine. Keep in mind, this probe is moving in parallel with the DoJ’s criminal investigation for money laundering and fraud. As one of the largest holders of BTC and the most dominant market manipulator in the global crypto market, it once again begs the question if the whole crypto industry is built on a house of cards. We continue to believe Binance may be in a similar company as FTX later this year.

Finally, over the weekend Binance temporarily halted BTC withdrawals multiple times citing “network congestion.” Curious timing. This is all to say – stay vigilant. We all want the next crypto bull market to come, but we need to eliminate the remaining rot in the industry before we have clear skies.

- Netizen Velez