2023 Will Be Worse

2023 Will Be Worse

Global Recession Likely a Late 2023 Event

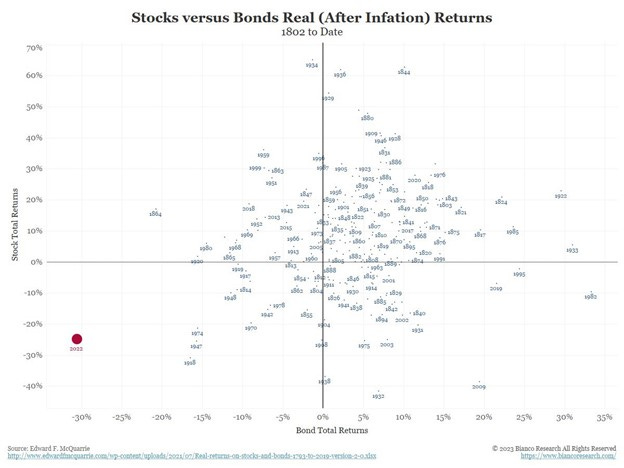

2022 Was Awful For Investors

In 2022, both stocks and bonds saw historic losses, as investors had nowhere to hide. Adjusting for inflation, U.S. long-term bonds dropped a staggering 30.2%, the worst we’ve seen on record dating back to 1793. Meanwhile, U.S. stocks saw an inflation-adjusted loss of 24.4%, the ninth-worst annual return in history. But the pain didn't stop there. Crypto investors also suffered, with Bitcoin prices dropping nearly 65% in 2022 and Ethereum prices falling by 68%. For context, 2022 was the worst year for Bitcoin since its 73% decline in 2018.

The weakness in asset markets was catalyzed by a historically hawkish Fed that came out swinging in November 2021 after “transitory” inflation remained more persistent than economists expected. As a result, the Fed is now fighting two wars: one against inflation, and the other to restore its credibility as an economic institution.

We believe 2022 was only phase 1 of this long bear market, characterized by a liquidity cycle downturn. As the Fed raised interest rates and began reducing the size of their balance sheet via quantitative tightening, liquidity began draining from global financial markets, causing the USD to strengthen and interest-rate sensitive assets (like stocks, crypto, and real estate) to fall in value. As the value of U.S. Treasuries continue to rise, higher “risk-free” interest rates will disincentivize investors from taking on incremental risk in stocks and crypto. As we move beyond 2H23, we believe phase 2 of the bear market will continue, and the global economy will begin to enter a credit cycle downturn, causing even further pain for businesses and investors.

In this letter, we’ll explore our base case, downside risk, and upside risk for the markets and economy, and then take a closer look at the state of the broader crypto industry.

Disclaimer: 2023 will see some changes to the Netizen substack. You can expect each publication to be shorter and less technical. All views will convey my medium term (3-12 month) thoughts, and I will try to keep concepts high level (when possible).

Base Case (High Probability)

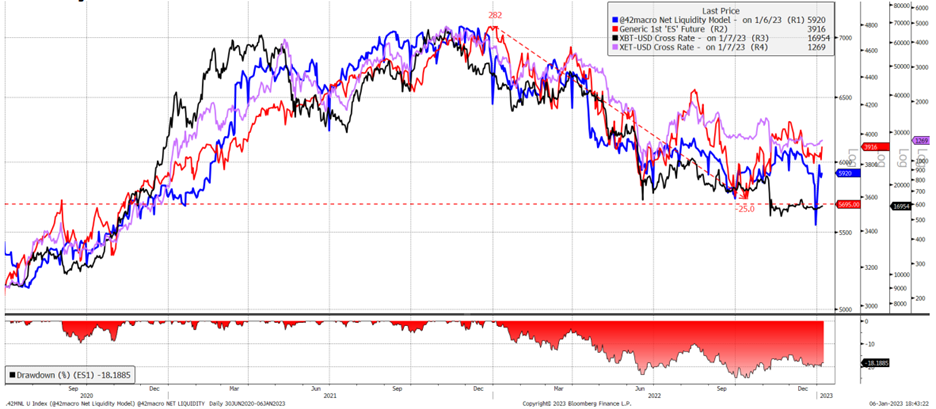

The Federal Reserve's December FOMC meeting was incrementally hawkish, extending phase 1 of the liquidity cycle downturn into 2023, with no stimulus likely returning until 2024. According to our models, this is negative for the S&P 500, and Ethereum, and in line with where Bitcoin is currently trading, as net liquidity is expected to be around $5.7 trillion by the end of 1Q23. As we move through the 2023 bear market, the biggest challenge for investors will be recognizing when the phase 1 liquidity cycle ends, and when the phase 2 credit cycle downturn begins. If the two cycles are far apart, expect vicious bear market rallies. If the two cycles happen consecutively, expect widespread fear and pain.

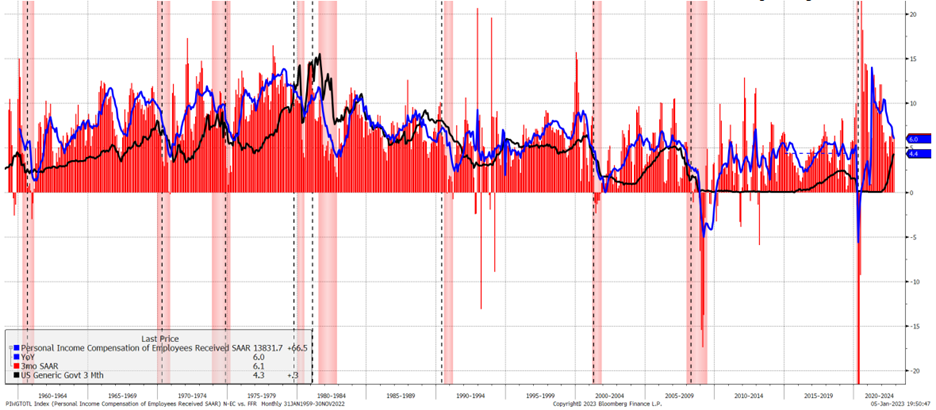

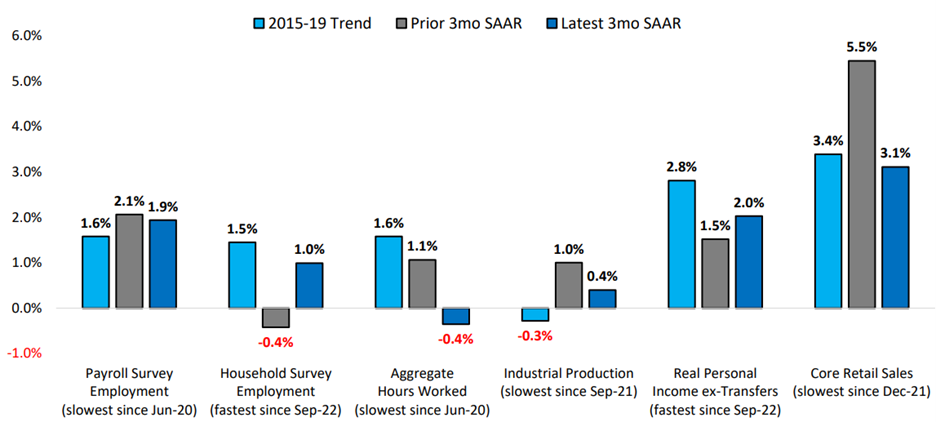

While the Fed has made progress on headline and core inflation, measures of underlying inflation, including the potential for a wage-price spiral, are beginning to rise. The Fed is now more focused on the labor market than inflation metrics, as evidenced by their upgraded language in the December FOMC meeting from needing "clear and convincing evidence" to pivot, to needing "substantially more evidence." This is due to the continued growth of nominal employee compensation, which is currently at 6.1% on a 3-month annualized basis. The Fed is aware that a wage-price spiral will exacerbate services inflation, which accounts for 82% of GDP and 86% of total employment. Historically, the Fed has had to raise the Fed funds rate (currently 4.25%-4.5%) above employee compensation to stave off a wage-price spiral.

Another factor giving us concern is the inversion in the 10Y3M yield curve, which currently stands at -105 bps. Notably, the 10Y3M yield curve is considered the most reliable recession indicator due to its 100% historical hit rate. However, our analysis suggests that the risk of recession is concentrated 12-18 months after inversion, meaning that a recession is more likely to occur in 4Q23 or 1Q24. This contrasts with the expectations of many investors and consumers predicting a recession in 1H23. Our perspective is that the labor market is more resilient than many people realize. Even though this recession may be the most predictable one yet, we expect it (in conjunction with the start of the phase 2 credit cycle) to happen in the latter half of the year, rather than in the next three months.

Our view is that the U.S. economy is much more resilient than the consensus believes, which, paradoxically, is negative for markets. This is because it gives the Fed more justification to continue tightening financial conditions. Strangely enough, an immediate recession would be the "bull case" because investors assume the Fed would quickly pivot to stimulate liquidity to support the economy and asset markets. Both households and corporations have enough juice to support the U.S. economy in the near term, as aggregate household balance sheets are in excellent condition, with $7.9 trillion in checkable cash – nearly $4 trillion more than before COVID. This is helping drive strong consumer spending, all while credit card debt as a percentage of disposable income remains at very safe pre-COVID levels. Meanwhile, corporate balance sheets are also in good shape, as there are no red flags yet in the form of higher interest rates or excess inventories.

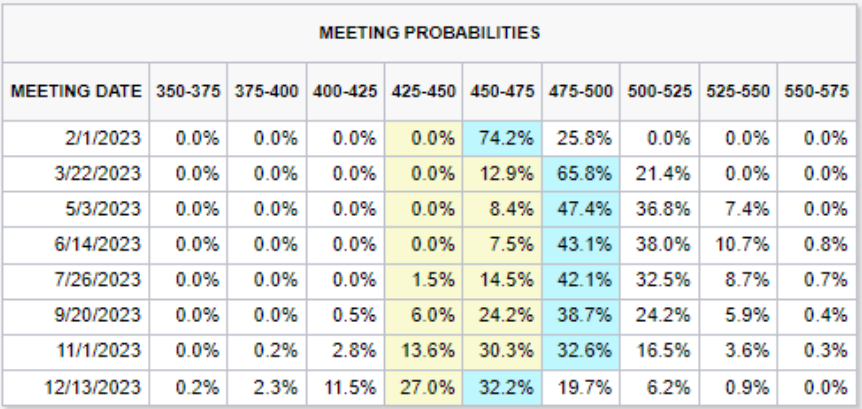

Overall, we believe that investors are misinterpreting the Fed's reaction function and policy expectations. Fed fund futures are pricing in interest rate cuts in mid-2023, which doesn’t align with the Fed's projections for a terminal fed funds rate of 5.1% by the end of 2023 and no cuts until 2024. Investors are complacent and don’t seem to have faith in the Fed's ability to tackle both inflation and regain credibility. As a result, we expect investors will gradually adjust their perception of the Fed's hawkishness as they come to understand that the economy is stronger than perceived.

Downside Risk (Medium Probability):

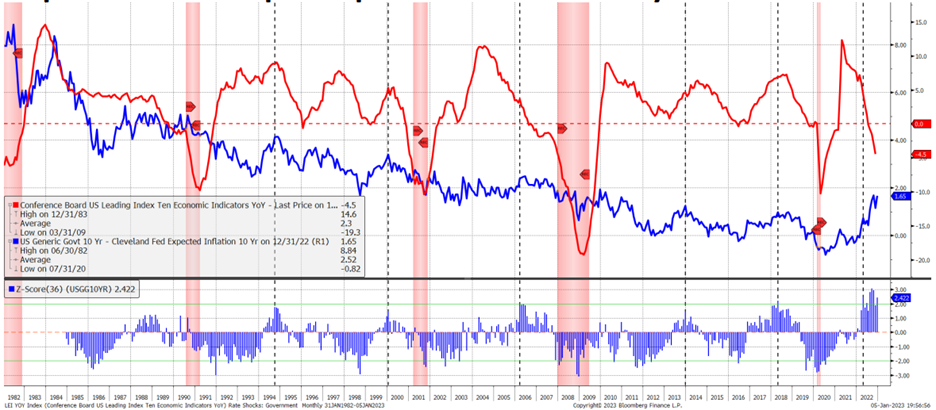

While our base case is bearish, there is potential for further downside risk to materialize in the market due to the rapid rise in interest rates seen in 2022. According to our analysis, this 3-sigma move in interest rates is leading to a sharp decline in the Conference Board's US Leading Index, which is used to measure future economic activity. Consumers also seem to be anticipating a recession, as evidenced by the negative difference between the Conference Board's Consumer Confidence Expectations and Present Situations Index – a level not seen since the COVID-19 pandemic and the 2000 tech bubble.

Additionally, the Federal Reserve's summary of economic projections implies a recession will occur by the end of 2023. Specifically, they expect core PCE to reach 3.5% by the end of 2023, even though this metric has never declined by 120 bps over 13 months without a recession occurring. The Fed also expects the unemployment rate (U3) to reach 4.6% by the end of 2023, but U3 has never increased by more than 110 basis points over 12 months without a recession happening.

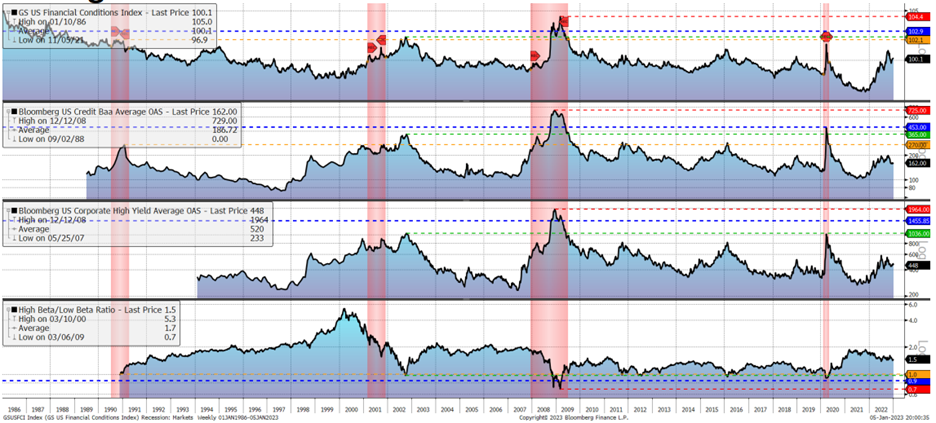

However, it seems that investors are not currently pricing in the possibility of a recession. Indicators such as the U.S. Financial Conditions Index, investment grade credit spreads, high yield credit spreads, and the ratio of high beta to low beta stocks do not show the same level of concern as seen in previous recessions, such as in 1990, 2000, and 2008. It’s important to note, however, that when a recession occurs, it will be the result of phase 2 (credit cycle downturn) – which occurs in all recessions. We generally see investors flee to safe-haven assets like U.S. Treasuries during proper phase 2 credit cycle downturns, as interest rates will be high enough and stocks will be unattractive.

Upside Risk (Low Probability):

One potential upside risk for the markets is the abrupt end to "zero COVID" in China. If China successfully reopens, this could lead to a positive shock for global growth and be bearish for the USD. This could also result in a GOLDILOCKS pain trade, given current market positioning and trending cross-asset correlations. In addition, capital outflows are a risk for the USD, as both net foreign capital flows into the U.S. economy and the U.S. net international investment position have recently declined. A weak USD could support global growth and carry trades, and allow the People's Bank of China to shift from supporting the renminbi to stimulating Chinese demand.

Another factor supporting markets is passive investing via retirement plans. It’s unlikely that the market will decline significantly until the labor market begins to weaken materially. As unemployment increases, the passive bid in equity markets will slow and eventually turn into a headwind for prices. While the buy-side has been bearish for most of 2022, working professionals continue to buy stocks on auto-pilot, supporting stock indices temporarily. We could call out, however, that this passive bid does not exist in the crypto market, except from hardcore Bitcoin holders who dollar-cost-average regularly.

It's worth noting that the Federal Reserve's pivots during bear markets are usually bullish for risk assets. On a median basis, markets tend to bottom about a month after an inflection in the liquidity cycle (pause or pivot). However, if the Fed pivots during a recession, it typically takes longer for markets to bottom so don’t be too quick to pull the trigger and buy if the Fed pivots during an actual recession.

Is Crypto A Criminal Enterprise?

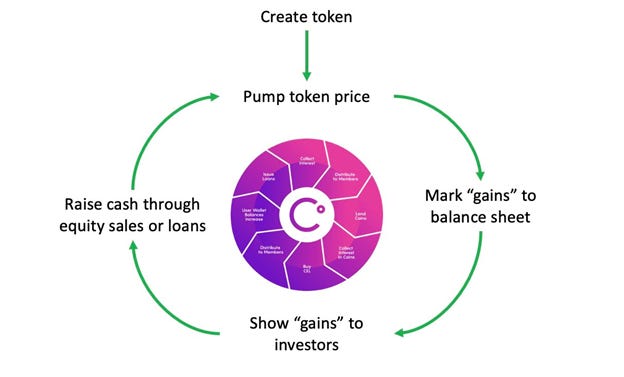

We want to spend the rest of this letter warning crypto investors about the potential for catastrophic risk in the crypto industry, which has been brought to light by the collapse of FTX and Alameda Research, as well as ongoing investigations into Binance, DCG, and others. According to James Block (author of Dirty Bubble Media), some of these companies may be involved in financial fraud and criminal activity, including money laundering and capital control evasion. Recall, the collapse of Terra-LUNA and Three Arrows Capital in May 2022 bankrupted BlockFi, Voyager Digital, and Alameda, and it's uncertain how many more crypto companies, hedge funds, and exchanges are now secretly insolvent.

Block suggests the small size of the crypto industry creates the potential for competitive collaboration between companies, which may lead honest actors to "turn a blind eye" to nefarious actors in the space. The close connections between companies such as FTX, Alameda, Tether, and Binance, as well as their ties to individuals, organizations, and governments, suggest that there may be a web of collusion within the industry. For example, Moonstone, which is connected to FTX and Alameda, has ties to Deltec Bank, the bank used by Tether, and the former general counsel of Deltec is now the Attorney General of The Bahamas (where FTX was headquartered).

Meanwhile, Binance, the largest crypto exchange in the world, is facing scrutiny over its proposed $1bn acquisition of bankrupt cryptocurrency lender Voyager Digital through its "independent" US exchange, Binance.US. The legal relationship between Binance and Binance.US has been questioned for years, and the SEC recently filed a limited objection to the proposal, leading some to believe that Binance.US may not be able to afford the acquisition without potentially receiving funds from Binance's global entity. In October, Reuters reported that Binance.US acts as a "de facto subsidiary" to insulate Binance from US regulators. If the SEC has enough evidence to suggest comingling of Binance and Binance.US funds, the entity may be exposed to an investigation.

Furthermore, there are concerns about the sustainability and artificial value of Binance's BNB coin, a digital asset native to the Binance ecosystem that is used to facilitate transactions on the platform. Created in 2017 by the cryptocurrency exchange, BNB's value is based on its demand as a medium of exchange and the perceived value of Binance as a company. According to Block, Binance owns 70-80% of the BNB market cap, similar to FTX's FTT token, and there are also concerns about the stability of BUSD as billions of dollars in stablecoins pegged to the US dollar on the Binance Smart Chain were not backed with real assets for extended periods.

Meanwhile, Barry Silbert, CEO of Digital Currency Group (DCG), and Cameron Winklevoss, CEO of Gemini exchange, are publicly fighting over the collapse of the Gemini Earn program. According to Gemini, DCG owes the company $900 million for funds that were lent as part of the Gemini Earn program but have not repaid the money, causing Genesis Trading (DCG’s subsidiary crypto lending company on the verge of bankruptcy) to fail to pay Gemini. Investors have filed a lawsuit against Gemini, alleging fraud and violations of securities laws because the Earn program was not registered and investors were unable to fully assess its risks.

This brings up further concerns about the sustainability of DCG’s crown jewel asset, the Grayscale Bitcoin Trust (GBTC), the largest publicly traded investment vehicle that holds ~633,000 BTC. The price of GBTC has been decreasing in value relative to Bitcoin and now trades at a 45% discount, meaning that for every $1 of GBTC an investor purchases, they receive $0.55 worth of BTC. There are also concerns about the stability of GBTC as it has been reported that DCG has been using the trust's management fees to repurchase GBTC and is now the largest owner of its investment product (sound familiar?) It has been speculated that DCG may need to liquidate its Bitcoin holdings to prevent its subsidiary Genesis Trading from bankruptcy, though no official announcements have been made.

This is all to say that the crypto industry is in deep trouble. We believe the FTX and Alameda collapse will uncover layers of greed, overleverage, and criminality in the coming months, as the SEC and DOJ will have carte blanche to regulate the entire space. While the fundamental value of Bitcoin remains unaffected, we view the rest of crypto as radioactive. Between incoming regulation, negative sentiment, forced liquidations, and decreasing liquidity, it’s unlikely Bitcoin and crypto will bottom before these overhangs are resolved.